It’s that time of year again! If you purchased a primary residence last year, make sure to file your homestead exemption with the county to save some money on your property taxes! You must submit this paperwork by April 30th.

Your Homestead Exemption will be denied unless all of the required documents show the same homestead address. First, fill out the application specific to your county, then mail all of the documents to the county appraisal district. Williamson County even lets you file the paperwork online! Download the residential homestead exemption application for your county by clicking the link below: Travis County Mailing Address: P.O. BOX 149012, Austin, TX 78714-9012 Williamson County Mailing Address: 625 FM 1460, Georgetown, TX 78626-8050 Hays County Mailing Address: 21001 IH 35 North, Kyle, Texas 78640 Bastrop County or Call 512-303-1930 ext. 22 Mailing Address: P.O. Box 578, Bastrop, TX 78602 Burnet County Mailing Address: P.O. Box 908, Burnet, TX 78611-0908 Llano County Mailing Address: 103 E. Sandstone St., Llano, Texas 78643 Include a Copy of your Driver's License or Identification Card: Your driver's license needs to be from the Texas Department of Public Safety (TX DPS) and the address must match the homestead address. Contact me if you have any questions!

0 Comments

If you’ve been renting for a while, I’m sure you’ve at one time considered the idea of buying a home. Yearning for a place where I could rip the carpet out, paint the walls whatever color I wanted, and replace the completely unpredictable electric oven was enough to propel me towards making my homeownership dreams a reality. For many people, thinking about buying your first home can seem like a daunting process. In fact, I talk to tons of people who never even considered a home purchase within reach due to the many misconceptions about the home buying process. Maybe you are one of those people who is absolutely sick of paying your landlord’s mortgage. You believe in the fallacy that you have to put 20% down on a home, and have succumb to the idea that you will be a renter for life. Luckily, I’m here to show you just how easy it is to buy a home. There are many options for purchasing a home with less than 20% down. There are even USDA home loans that you can obtain for rural homes for 0% down, and a number of local and state programs aid first-time home buyers with various initiatives including down-payment assistance programs. Your first step towards buying your first home in Austin, is to talk to a lender to determine your home budget. In fact, I recommend you talk to a few. Check to make sure you are getting the best rate possible, and find someone you enjoy working with. Feel free to reach out to me for specific lender recommendations for your needs. Before you start talking to lenders, it is important to gather at least some of the documents your lender will need. Preliminary documents include: w2s, past two years’ tax returns, pay stubs, past two months’ bank statements. A list of ongoing monthly debts such as student loans, car payments, and minimum balances for credit cards is also helpful. Your lender many need additional documents based on your unique situation; however, having these items handy will give you a good head start.  Once you submit those documents to the lender of your choice, you will be given a pre-approval letter that notes the maximum loan amount or the maximum amount you can spend on a home. Now, it’s time for the fun part! You will probably have given a little bit of thought into what you want in a home before this stage. Now, you will refine your needs, determine your must-haves, and start house-hunting. Your dedicated REALTOR, yours truly, will help you locate homes that match your criteria, and tirelessly point out the pros and cons of each home. Eventually, we will find the one! When we finally locate the perfect place, the one that is destined to be your future abode, and makes you feel all warm and fuzzy inside, I go into energizer bunny mode. We will determine the best price to offer, discuss if you’d like the washer and dryer to stay with the home, determine if you’d like a home warranty to be included with the purchase, and assess all the other details of the contract. I’ll write up the contract as discussed, shoot it over to you for signatures and then we will submit the offer. If it’s a hot home with lots of interest, we may even craft up sweet letter about how this home is just perfect for you and your golden retriever puppy, Bo. Usually, within less than an hour after deciding you wanted that perfect home with the white picket fence, your offer is in the hands of the listing agent. Once the listing agent receives the offer, she will present it to her clients. They may decide to make some adjustments in which case, we would go back and forth negotiating for what’s best for you but also agreeable to the seller. Or, they may simply accept the contract as is. Regardless, once the contract is agreed upon by both parties, your option period starts. The option period is a set amount of days that you, the buyer, has to do your due diligence on the home and back out if you find anything too scary. We will discuss the exact length of the option period when writing up the contract but usually it’s around 5-10 days. I’ll send you recommendations for inspectors, and we will schedule one to come out and thoroughly evaluate the home. I’ll meet with him after to discuss the findings, and if possible I highly encourage you, my clients, to come too.  After the inspection, we will discuss the results. If there are repairs that need to made to the home, we can either request that the repairs are made prior to the closing date, or request that the sellers give money for the repairs at closing. Ultimately, this becomes another back and forth situation which cumulates in an official amendment to the contract. Along the same time, that we are reviewing the results of the inspection, the lender is working to order an appraisal on the home. For the home buyer, this is not really a hands on part of the process. The lender will notify you that the appraisal has been ordered and will let us know when it comes back, hopefully at or above the offered value. At this stage, there is a slight lull in the process. At the beginning, your moving quickly looking at homes, writing offers, negotiating. Now, you’re mostly waiting. Waiting for the appraisal to come back, and you may be submitting additional documents to your lender. Once your lender has the appraisal and all outstanding documents, your file is submitted to underwriting. At this point, you will choose a home insurance policy, a home warranty if you’d like one, and eventually you will hear the sweetest words you’ve been granted “clear to close”. The day before closing, or the morning of, it’s always prudent to do a final walk-through. You will want to see with your own eyes that the home is in the agreed upon condition, and that any repairs negotiated during the option period have been completed to your satisfaction. The next stop is the title company where will you sign your life away, and become a proud first time homeowner. Unfortunately, you don’t usually get the keys right away.  Once you’ve signed everything, the documents are sent back to the lender and as soon as the loan funds, you get the keys. This usually takes a few hours, so if you’re so inclined, I’d highly recommend a spontaneous mid-day happy hour to celebrate your new status as a proud first time home buyer. After a few margaritas, or maybe a bottle of champagne, the time flies by. Suddenly a consistent vibration or an ascending chime disrupts the chatter; upon answering you find an upbeat title employee telling you the time has finally arrived. Now, you can pick up the keys to the place you will call home.

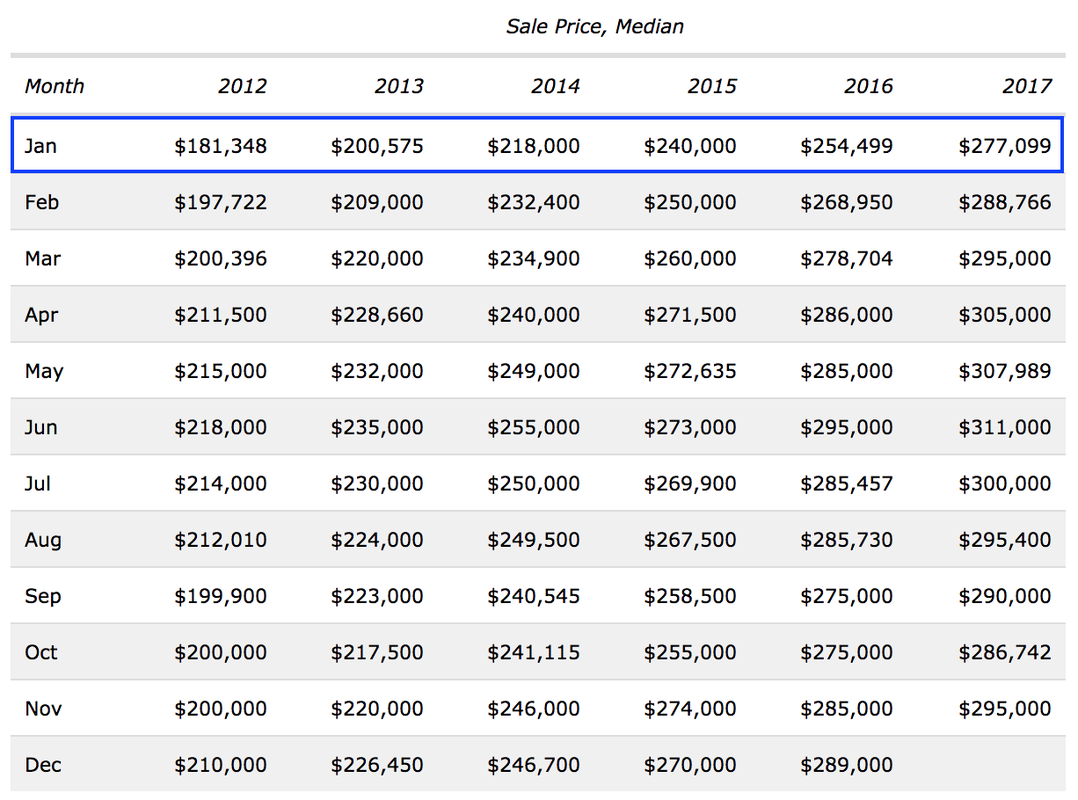

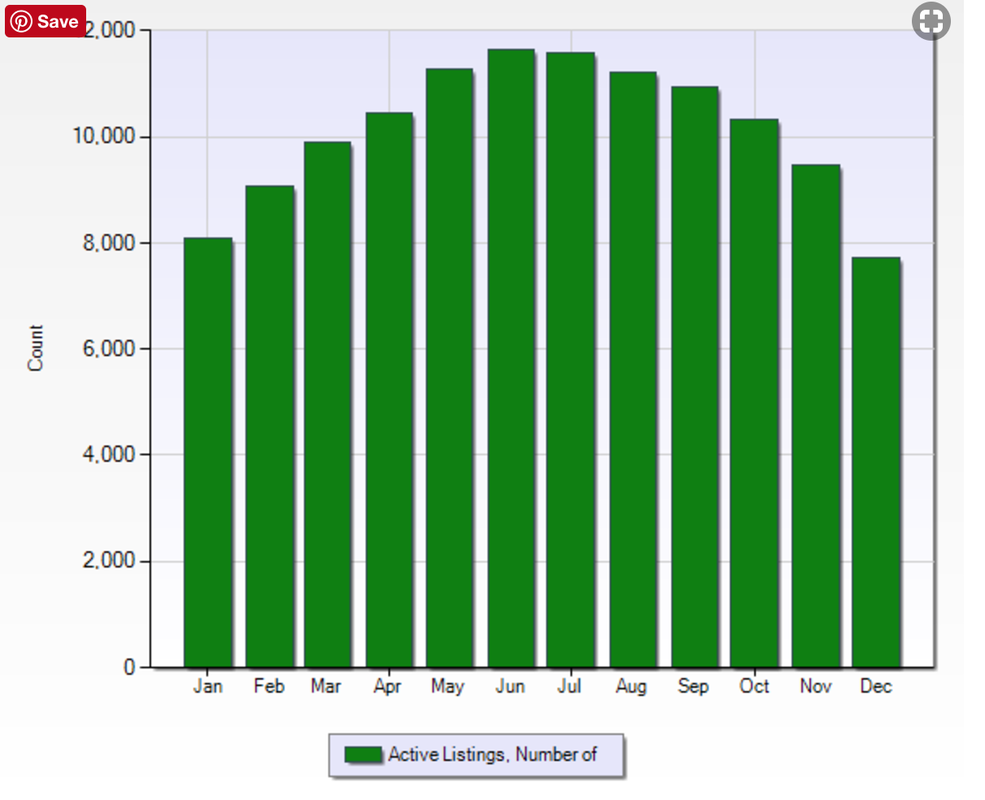

If you’re sick of renting, and ready to take the plunge into home ownership, contact me today, I’ll show you just how easy it is to buy your first home in Austin, Texas.  If you’ve been on the fence about purchasing a house in Austin, now is the time to take the plunge and start looking at homes. According to data from the Austin Board of REALTORS, the lowest median sales price for Austin area homes occurs in January. This trend has remained consistent for at least the past 5 years. For a home sale to close in January, that usually means the home is going under contract in December. Thus far in 2017, the highest median monthly home price in the greater Austin area for single family homes occurred in June when the median sales price was $311,000. Compare that to this year’s January median sales price of $277,099, and it’s obvious why closing on a home in January is when you get the best deal.  If January historically yields the lowest median sales price on Austin area homes, you may be wondering why I’m suggesting you should be looking at homes now. Well first of all, finding the right home may take some time. Rarely, do buyers I work with fall in love with the first home I show them. Side note: this has occurred before and if you have a clearly defined sense of what you are looking for in a home and can articulate this thoroughly, it can vastly shorten the shopping time. In general, though, it usually takes time to find the perfect property. The second reason you should be looking now, is that the majority of home purchasers are obtaining a home loan. These take time, and most lenders need 21 days from the date the contract is agreed upon by all parties to the closing date. You may be wondering why January continually yields the lowest median home sales price. Well, this is for a variety of reasons; however, this is primarily a matter of supply and demand. There is far less demand for homes in January as opposed to June. Most people are not thinking of purchasing a home around the holidays; conversely, many families time moves around the school year. Thus, home sales volume, and home sales prices skyrocket in June. There is one disadvantage to looking for a home in December. There is less inventory in December than any other month. Last December, there were 7,714 single family homes active on the MLS in the greater Austin area. In May of 2016, there were 11,267 active homes.  The numbers don’t lie. Now is the time to get the best deal on an Austin area home. If you’re ready to start looking, you can view all Austin area homes for sale here, or contact me today, and I can simplify the process for you.  If you’re like me, a steady marathon of Chip and Jo’s Fixer Upper, leaves me yearning for a flip of my own. Tear down some walls, add some shiplap and large beams, tear out the ugly carpet, and you have a dream home anyone would want to live in. If you’re planning to personally live in the home, a fixer upper offers the opportunity to customize the house to your unique design specifications. By putting in the work, you will spend less money and have a nicer home than if you were to buy a home that someone else already took the time to remodel. Whether you are looking for a fixer upper for a quick flip or a permanent home, Austin has a wide variety of fixer uppers ripe for renovations. Take a look at these 5 Austin area homes that with a little TLC could be true show stoppers. 1. Large East Austin Home with Guest Unit

2. Great North Austin Home on Private Lot, Easy Access to Mopac

3. Westlake Estate on Nearly 2.5 Acres with Sprawling Views of Barton Creek

4. Conveniently Located South Austin Home

5. Central Austin Fixer Upper, Walking Distance From South Congress Strip

If you’d like to see more fixer uppers, you can search all Austin area homes for sale here or contact me today for specific recommendations.  In a Texas real estate transaction involving third party financing, ie. a loan, lender approval is required for the deal to close. That approval is broken down into two parts. The buyer must obtain approval for the loan based on their finances, credit, income etc. and the property must also be approved. Physical conditions within the home may cause the property to become ineligible for funding, or the home may not appraise at the value agreed upon in the contract. For the purpose of this post, I am focusing on the latter: what happens when a home doesn’t appraise.

If an appraisal comes in at a lower value than the agreed upon contract price, there are a few options for how the parties to the contract can handle this scenario. In order to illustrate these scenarios, let’s say that the Johnsons are selling their home to the Smiths. They have agreed to a purchase price of $360,000; however, the home only appraised for $340,000. The first option is that the sellers and buyers can agree to drop the contract sales price to the appraised value. However, the Johnsons may not want to just drop the price to $340,000. After all, they accepted the Smiths offer in a multiple offer situation, and they turned down a $350,000 cash offer. So, let’s say the Johnsons do not agree to reduce the sales price to $340,000. This brings us to scenario number two; the Johnsons propose that the Smiths bring $20,000 cash to the table in order to close the deal at the agreed upon $360,000 sales price. If the Smiths are capable of coming up with an additional $20,000 cash to put down on the property, this solution could work. However, the Smiths are not obligated to agree to this scenario even if they are financially capable of it. Let’s say the Smiths only have an additional $10,000 they could put towards the home. The Smiths could propose that they put an additional $10,000 down, and that the sales price is reduced to $350,000. If the Johnsons approve, this scenario would also allow for the transaction to close. If the Smiths and the Johnsons cannot come to an agreement, the deal will fall through and the earnest money will be returned to the Smiths. The third party financing addendum used in Texas real estate transactions is very clear on this. However, there is one other option for the Johnsons and Smiths in this situation. They could appeal the initial appraisal, or request a new appraisal. It would be prudent for the Johnsons to make sure that the Smiths would still pay the agreed upon contract price of $360,000 if a new appraisal deems the property to be worth that amount. Many buyers are inclined to not pay more than the appraisal amount, and in Texas, they are protected from doing so unless they want to bring the extra cash to the table.  If you are considering buying a home, it’s highly likely that you are looking at homes on Zillow. Zillow spends exorbitant amounts on advertising, and their platform is incredibly user-friendly. While Zillow may be great for casually browsing homes, it’s not the best platform when you are seriously contemplating what property to buy.

First it is important to know how Zillow works. The majority of listings appearing on Zillow are syndicated listings from the Boards of REALTORS for that specific area. There are a few other types of listings that appear on Zillow, and I will discuss those later. Real estate agents list homes using their local boards of REALTORS multiple listing service (MLS). Agents are responsible for entering all information about a given property into their MLS, and then are given an option if they would like to syndicate the listing to third party sites such as Zillow. There are three key components to understand here. First, all information that is eventually appearing on Zillow about a particular home was most likely manually inputted or at least verified by an agent. This leaves room for human error. I have seen homes advertised as 3 bedrooms that really only have 2, homes where the square footage is completely wrong, and homes that are really located in one area of town being displayed on the map in an entirely different county. Second, not all listings that are on the MLS are on Zillow. Real estate brokerages choose what sites, if any, their agents are allowed to syndicate their listings to, and when imputing each listing, agents are given the choice if they want to syndicate that particular listing to third party sites. Third, syndication takes time. The most common example of this I see is a buyer who is interested in a home they saw on Zillow as an active listing. When they call me about the property I must tell them that the home is actually already under-contract and Zillow is simply behind. Additionally, all of the information available on the MLS is not syndicated to Zillow. Only a portion of all of the data entered in the MLS is syndicated to Zillow. In the MLS, agents can view documents associated with the property such as important information about the condition of the home, information about improvements, or a property survey. Zillow also doesn’t tell you if the property is located in the flood zone, an important component to consider when looking at purchasing a new home. While Zillow does show you some history in regards to the prior sales associated with the property, it doesn’t tell the full story. Not all listing activity is displayed, and it doesn’t necessarily show you when major improvements were made or how a property was actually listed 3 different times in the past year and has still not sold. Another common occurrence I see is properties that are technically condos being listed as homes. In fact, I see this on the MLS as well. It has become increasingly popular to subdivide lots, and build two homes on one lot and then legally separate the two buildings with a condo regime. You also see stand-alone condo communities where the property is listed as a home. In both of these cases, the property does appear to be a single family residence but is technically a condo. It is important to know when you are looking at a condo because financing options, restrictions, and appreciation will differ from those associated with a true single family home. The other types of listings you see on Zillow are For Sale By Owner, Make Me Move and Builder Listings. For Sale By Owner and Make Me Move listings are both owner curated listings. While the Make Me Move listings are less definitive (the owner is merely testing the waters to see if they can get a given amount for their home), both listing types tend to be vastly over-priced and may or may not be up to date or contain completely accurate information. With all three of these listing types it is common for them to become forgotten. Owners and builders alike appear to list homes on Zillow and then forget they were there. I have called owners who no longer have any intention of selling, and builders whose property sold months ago but they forgot to take the listing down. Whether you are looking at homes on Zillow or straight from an agent’s portal to the MLS, you cannot be entirely sure all the data you are being show is 100% accurate. It’s important to have a trusted real estate agent representing you. They will notice when a figure doesn’t look quite right and will perform the necessary due-diligence on your behalf to make sure you are getting what you pay for. Furthermore, they will make sure you don’t waste your time looking at homes that are no longer even listed for sale or that don’t actually meet your criteria. If you are looking for an all-star agent in the Austin area to make your home buying process as easy as possible, call me today at 512-779-7597 or visit my website to learn more about my buyer representation services.  As you may recall, in my previous blog post titled, When’s The Best Time to List My Property, I mentioned how most families prefer to move during the summer. This has resulted in sellers getting the highest price for their home in May/June. In fact, over the past five years, we have consistently seen the highest median sales price for homes in the City of Austin occur in either May or June. Given that the average days on market for Austin properties over the past five years that sold in May or June ranges from 32-45 days, and the fact that a home usually takes on average 30 days to close after going under contract, these properties were likely listed for sale in March or April. Thus, if a home that was listed for sale in the early spring is still available, it may be a great opportunity to get a home for a steal. You may have hesitations about looking at a home that has been on the market for over 100 days, and wonder why this home hasn’t sold. You might think something must be wrong with this home. However, it may have simply not been marketed properly, been priced too high initially, or this could be a result of one of these other reasons. Regardless, if a home was listed in the early spring and is still on the market, the sellers may be getting anxious to sell. This is especially true if the home is vacant. A vacant property means the sellers are simply incurring costs (utilities, property taxes, insurance, mortgage etc.) without any benefit. After a few months of this, many sellers become more inclined to accept a lower offer. If you’ve been looking for a home in Austin throughout the spring and early summer, you know how competitive the market has been. Multiple offers on homes occurred frequently, and you may have become burned out by the process. Now, there is less competition. In fact, data from the Austin Board of REALTOR’s MLS shows price decreases are occurring on many Austin homes. Everyone knows that moving in Austin this time of year can be hot. However, a little sweat may be worth it if you can get a great deal. If you’re looking for a great buy in Austin, contact me today. I can easily locate the best options for you based on your specific needs. If you feel like looking at Austin homes for sale on your own first, click the link below.   My Austin clients frequently have questions about who pays for what in a real estate transaction. In Texas, almost everything is negotiable; however, there are certainly norms and the promulgated forms used by Texas REALTORS naturally lend way to certain cost distributions.

In order to think about who pays for what is a real estate transaction, you first most consider what expenses are involved in a real estate transaction. One of the largest expenses in a real estate transaction is commissions. In Texas, real estate commissions are customarily a seller expense. It is most common to see the seller pay six percent of the sales price towards commissions, three percent to the buyer’s broker and three percent to the listing broker. However, this distribution is not set in stone. For multi-million dollar listings, the commission may be lower, and the seller ultimately determines the commission percentage as well as the distribution between the buyer and the listing brokers. Additional costs involved in a real estate transaction include marketing expenses, title policies, appraisals, surveys, inspections, energy audits, and loan origination fees. Good listing agents will usually take on the marketing expenses incurred to properly advertise a property. These expenses include professional photography, print marketing (including mailers), digital marketing platform expenses, and advertising fees. Staging fees may be paid for by the seller directly or the listing agent. The owner’s title policy usually costs a little more than one half of a percent of the sales price. Click here for exact title policy costs in Texas. The owner's title policy is typically a seller’s expense. However, with the competitive buying market it is not uncommon to see buyer’s incurring this cost to make their offers more appealing to the seller. The lender’s title policy cost is related to the loan amount for the property and is typically a buyer expense. Property inspections are a prudent decision for any buyer. These inspections can cost several hundred dollars, and additional specific inspections for items such as wells, septic systems, foundations, etc. may be needed as well. These inspections usually occur during the option period at the expense of the buyer. In certain situations, it may be beneficial to have a property pre-inspected. In this case, the inspection would be a seller fee. Lender related fees are typically paid for the buyer. In addition to the lender’s title policy, buyer costs associated with loans include loan origination fees and appraisal fees. These fees will vary based on both the property and the lender utilized. A survey is generally required for the sale of property in Texas. If the seller has an existing survey for the property, it may be used for the sale if it’s approved by the lender and the title company. The Texas Real Estate Commission’s 1-4 Family Residential Contract offers 3 options for how the survey will be obtained. Option 1: an existing survey will be used and it if is not approved by lender/title company you can elect for the seller or the buyer to pay for a new one. Option 2: seller pays for a new survey. Option 3: buyer pays for new survey. A condo does not require a survey for a real estate deal. However, there will be other fees associated with a condo sale. When you are involved with the sale of a TX condo, you will want to consider who is going to pay for the resale certificate and who pays for the transfer fees. Again, the Texas condo contract is written in such a way that lends way for the buyer to pay for at least a portion of the transfer fees. Thus it is common for the seller to pay for the resale certificate and the buyer to pay for the transfer fees but this in no way set in stone. Both fees are entirely negotiable. If a home warranty purchase is noted on a real estate contract, it is likely an expense to the seller. This part of the real estate contract states that the seller will reimburse the buyer X amount towards the cost of a residential service contract. Escrow fees, the fees paid to the Title Company, are typically split between the buyer and seller. You may also see legal fees, processing fees, and various fees imposed by municipalities on either side of the closing document. This list is by no means exhaustive. There are a variety of fees involved with a real estate transaction and who pays for what is usually negotiable. If you’re a buyer in a competitive market, the more “typical seller-related expenses” you agree to take on, the stronger your offer will appear to sellers. If this all appears to be a bit much to take in and you’d like someone to walk you through the details or if you have additional questions, contact me today.  Are you considering buying a home in Westlake? If you are looking at houses for sale in Westlake, it is important to understand the Westlake housing market. Most people refer to Westlake as all of the homes that feed to Westlake High School. In fact, there are many mini-neighborhoods that make up the greater Westlake area. Houses in the Westlake area tend to be some of the most expensive houses for sale in the Austin area. This is primarily due to the fact that houses for sale in Westlake allow access to one of the best school districts in Austin, EANES ISD. If you have kids and are looking for houses for sale in Westlake, it is important to know which areas feed to which middle schools. There are two middle schools that feed to Westlake High School, Hill Country Middle School and Westridge Middle School. Homes that are located east of Loop 360 are in the MLS area 8E and these Westlake houses feed to Hill Country. Houses west of Loop 360 are in the MLS area 8W and these homes feed to Westridge.  This is important to know. If you are looking at homes for sale in Westlake Hills, you will find many affordable options in the Lost Creek neighborhood. This neighborhood is way closer to Hill Country Middle School, but houses in Lost Creek feed to Westridge Middle School. This means if you have younger kiddos and buy a house in Lost Creek or the Woods of Westlake, they will have a much longer commute during their middle school years.

Westlake houses for sale in the 8E area tend to be a bit pricier than those in 8W since these houses are also closer to downtown Austin. In 2016, houses for sale in the 8E area of Westlake had a median sales price of $1,031,750. Conversely, homes for sale in 8W sold for a median price of $725,000 in 2016. When you are considering buying a home in Westlake it is important to understand these intricacies of the Westlake area. You also want to look at the tax rate in different neighborhoods as these can vary substantially. Take a look at this post on tax rates in the Austin area if you are looking at houses for sale in Westlake. Still wondering where the best house in Westlake for your family is located? Give me a call today and we can discuss your exact needs and identify the best house for sale in Westlake for you and your family. Ready to start looking at houses for sale in Westlake, click here to view homes for sale in Westlake's 78746 zip code.  As Austin home values continue to rise, I’m often asked by prospective buyers if they should wait till the market turns to buy. Truthfully, no one can predict what the market will do. However, these days, my advice is usually no. Everyone knows Austin is amazing. More people are moving here every day. We have a healthy local economy full of growing businesses. We have a great culture, and beautiful outdoor spaces. We have universities that attract students, who often stick around - choosing to call Austin home. All of these reasons result in a steady influx of residents, and the available housing stock struggles to keep up with demand. There once was a time when I told people who were considering renting for another year to go ahead and renew the lease, call me when you’re ready to buy. That time has passed.

If you can afford to buy a home now, do it. Even if you have concerns about how long you will live in it, you can likely sell for a profit a few years down the line or rent it out while you wait for it to appreciate more. I have worked with a handful of sellers this year who only purchased their homes a few years ago and profited more than 50k when they sold. One of these clients even used a USDA loan and bought the property with 0 down. If you’re still on the fence, consider these market trends. The median sales price for a home in the city of Austin was $395,000 in May of 2017. The median price for an Austin home in May of 2016 was $364,978. From 2013 to 2017 the median sales price for Austin homes has increased well over 100k. Interest rates are expected to rise. Interest rates have been extremely low recently, and experts agree they are likely going to rise in the near future. A 1% increase in your mortgage rate equates to about 40k for a 30-year mortgage on a 200k property. If you’re considering buying in the near future, you should discuss locking in your rate now. If rising home prices and interest rates still haven’t convinced you to dive head first into a home purchase, consider this. If you pay $1,500 in month for 4 years, you have paid your landlord $72,000. Consider this coupled with the appreciation stats mentioned earlier and you can see how there is no better time than now to take the plunge! |